GENWORTH FINANCIAL (GNW)·Q4 2025 Earnings Summary

Genworth Q4 2025: EPS Misses as LTC Insurance Drag Continues, Stock Falls 5%

February 24, 2026 · by Fintool AI Agent

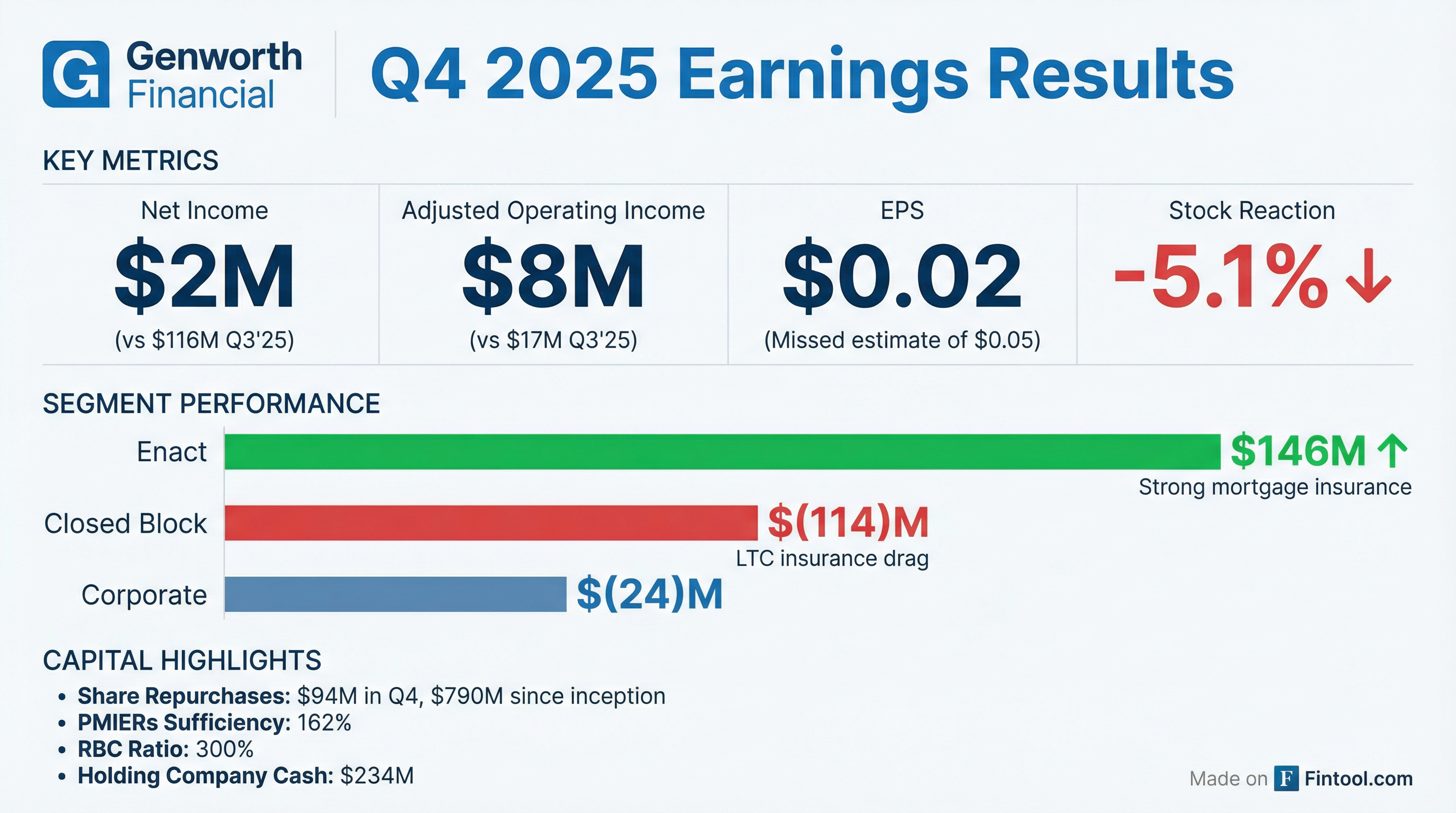

Genworth Financial reported Q4 2025 results that disappointed investors, with adjusted operating EPS of $0.02 missing consensus estimates of $0.05 . The stock fell 5.1% to $8.30 as persistent losses in the long-term care (LTC) insurance segment offset strong performance from the Enact mortgage insurance business .

Did Genworth Beat Earnings?

No. Genworth missed on earnings:

The sharp miss was driven primarily by the Closed Block segment, which posted a $114M adjusted operating loss compared to expectations of more modest deterioration .

How Did the Stock React?

GNW shares dropped 5.1% to $8.30 on February 23, 2026 — the largest single-day decline in several months.

The stock had been on a steady climb over the past two years, rising from $6.05 in early 2024 to nearly $8.85 in early 2026 before this earnings report reversed the trend.

What Changed From Last Quarter?

The key deterioration came from the LTC insurance business, which saw:

- $124M unfavorable A/E variance — higher claims and lower terminations

- $47M unfavorable assumption updates — benefit utilization and healthy life mortality updates

Segment Performance Deep Dive

Enact: The Bright Spot ($146M)

Genworth's ~81% stake in Enact Holdings continues to be the primary value driver :

Enact benefited from a $60M pre-tax reserve release driven by favorable cure performance and lowered claim rate expectations . The company also announced a new $500M share repurchase program and an excess of loss reinsurance agreement covering the 2027 book year .

Closed Block: LTC Continues to Weigh ($(114)M Loss)

The legacy insurance block remains a persistent drag :

LTC Insurance Analysis:

- Unfavorable A/E of $124M — higher claims as the block ages, with claim incidence increasing as policyholders approach peak claim age

- Assumption updates of $47M unfavorable — benefit utilization and healthy life assumptions updated to reflect near-term experience

Positives were noted in Life Insurance (+$15M from interest rate assumption updates) and Annuities (+$25M from mortality assumption updates) .

Capital Allocation & Shareholder Returns

Genworth continues executing an aggressive capital return program :

Holding Company Liquidity:

- Cash & liquid assets: $234M at quarter-end

- Includes ~$127M held for future obligations

- Received $127M in capital returns from Enact in Q4

What Did Management Guide?

Management provided detailed 2026 guidance on the earnings call :

Management noted that LTC A/E losses averaged $75M per quarter in 2025 and "could continue to see losses at this level in 2026," though with seasonal variation (more favorable Q1 from higher mortality) .

CareScout: The Growth Bet

Genworth continues investing in its aging care services platform :

Key Developments:

- Acquired Seniorly for ~$15M, expanding reach into direct-to-consumer market and senior living

- Care Assurance now live in 40 states — worksite and association group offerings planned for later 2026

- Care plans now available nationwide (both in-person and virtual)

- Expected CQN claim savings benefit: $1B-$1.5B NPV in closed block

Management Commentary

CEO Tom McInerney emphasized the strategic progress despite the LTC drag:

"Genworth delivered strong results in 2025 as we continued to execute against our strategic priorities. We took major steps to advance CareScout's strategy, with nationwide expansion of the CareScout Quality Network, the launch of Care Plans, and the launch and continued buildout of our CareScout insurance offerings."

AXA Litigation Update

The U.K. High Court case represents a potential upside catalyst :

Management noted the recovery is not taxable and not factored into capital allocation plans. If received, proceeds will be deployed toward CareScout investment, shareholder returns, and debt reduction .

Q&A Highlights

On the CareScout Strategy (Services + Insurance Together):

CEO Tom McInerney explained the full value chain approach :

"CareScout is the only LTC competitor that can deliver the full value chain in the LTC ecosystem... CareScout Services' target market is the 70 million baby boomers, 95% of whom never bought LTC insurance."

The strategy leverages CareScout Services to reach baby boomers needing care today, while building insurance products for their children and grandchildren who are witnessing LTC costs firsthand. Current costs: $76,000/year for home care and $125,000 in some markets for nursing home care .

CareScout Quality Network offers ~20% discounts from providers to make care more affordable .

Key Risks & Concerns

- LTC Tail Risk — Peak claim years still over a decade away; paid claims expected to continue increasing

- Rate Action Dependency — Requires continued regulatory approval for premium increases; $209M approved in 2025 (lower than prior years); ~$5B remaining value to achieve

- Assumption Volatility — Quarterly A/E losses averaged $75M in 2025; could persist at similar levels in 2026

- CareScout Investment Phase — ~$50-55M investment planned in CareScout Services in 2026; breakeven will "take time to scale"

What to Watch Next Quarter

- Q1 2026 LTC Experience — Management noted Q1 typically sees favorable mortality; will A/E variance moderate from $75M quarterly average?

- CareScout Match Progress — Targeting 7,500 matches for full year 2026

- AXA Appeal Outcome — Hearing July 21-23, 2026; potential ~$750M recovery

- Enact Capital Returns — Expecting ~$405M for full year 2026

- Care Assurance Distribution — Worksite and association group channels launching later in 2026

Full Results Summary

Values retrieved from S&P Global and company filings.